In 1990, a movie ticket cost about $4.50. A dozen eggs ran roughly 99 cents. A first-class stamp was 25 cents.

Today, those same things cost two, three, sometimes four times as much — and your retirement portfolio has had to keep up the whole way.

I still remember piling into our Ford Mustang convertible as a young girl, waiting in those long gas lines that snaked around the block. It was the 1970s energy crisis, and depending on whether your license plate ended in an odd or even number, you could only fill up on certain days. Nobody had to explain inflation to our family. We lived it.

Inflation isn’t a hypothetical risk for retirees. It’s a lived reality — one most of us over sixty have experienced more than once. And for people who depend on a fixed pool of savings to last 20 or 30 years, it’s one of the most important financial forces to plan around.

That’s exactly what Treasury Inflation-Protected Securities — TIPS — are designed to help with. Not flashy, not complicated, but purpose-built for one of retirement’s most persistent challenges: making sure your income keeps up with your life. TIPs serve as a foundational component of the portfolio meant to provide stability, purchasing-power defense, and high-quality diversification.

1. What are TIPS

Treasury Inflation-Protected Securities are U.S. Treasury bonds whose principal value adjusts with inflation.

Unlike a traditional Treasury bond, which pays a fixed principal amount at maturity, TIPS are structured so that their principal rises when inflation rises and can decline if inflation falls.

Here is how they work:

- TIPS pay a fixed coupon rate

- But that coupon is applied to an inflation adjusted principal balance

- As inflation rises, the principal value rises

- That means interest payments can also rise over time

- At maturity, investors receive the greater of the original investment or the adjusted principal

In practical terms, TIPS are one of the few mainstream fixed-income instruments specifically designed to help investors keep pace with inflation.

For retirees, that feature matters. Inflation may not dominate every year, but over a 20- or 30-year retirement, it can quietly do enormous damage.

2. Why TIPS Matter for Retirees

One of the greatest threats to retirement is not always a market crash. Sometimes it is simply this:

The cost of living rises faster than your income.

That is a serious risk for retirees because many retirement expenses are not optional:

- Food

- Housing

- Utilities

- Insurance

- Healthcare

- Transportation

A portfolio built only around nominal income can appear stable while losing real purchasing power over time. That is why TIPS can be valuable. They help retirees address a very specific problem:

They provide income and principal support that adjusts with inflation.

That makes them especially useful for investors who want part of their fixed-income allocation dedicated not just to income, but to real income — income measured after inflation.

TIPS may be particularly attractive for retirees who:

- Worry about the long-term effects of inflation

- Want a high-quality government-backed bond allocation

- Prefer lower-credit-risk fixed income

- Want to diversify away from purely nominal bonds

They are not a complete fixed-income solution on their own. But as part of a retirement-income foundation, they can be highly effective.

3. The Main Advantages of TIPS

TIPS offer several distinct benefits for retirees.

A. Direct inflation protection

This is the headline feature.

Unlike most bonds, TIPS are explicitly designed to help preserve purchasing power. If inflation rises, the principal value of the bond adjusts upward.

That makes TIPS one of the cleanest tools available for hedging unexpected inflation.

B. U.S. government backing

TIPS are issued by the U.S. Treasury, which means they carry minimal credit risk relative to most other income-producing securities.

That makes them a strong candidate for the foundational layer of a retirement portfolio.

C. Diversification within fixed income

Many retirees think of “bonds” as one category, but different bond sectors behave differently.

TIPS do not always move in lockstep with:

- Traditional Treasuries

- Investment-grade corporates

- Municipals

- Agency mortgages

That can make them a useful diversifier inside the bond allocation itself.

D. Potentially rising income stream

Because TIPS principal adjusts upward with inflation, the coupon payments may also increase over time.

That can help retirees maintain income purchasing power in a way many traditional bonds cannot.

4. The Risks and Limitations

TIPS are useful — but they are not perfect. Like every retirement income asset, they solve some problems while introducing others.

A. Lower starting yields than some alternatives

TIPS are often purchased for inflation-adjusted return, not for headline income. That means their starting yield may appear lower than:

- Investment-grade corporate bonds

- High-yield bonds

- Preferred securities

- Dividend stocks

For retirees focused purely on current cash flow, TIPS may initially feel less compelling.

B. Interest-rate sensitivity

Like other bonds, TIPS can decline in price when real interest rates rise. This is important: many investors assume TIPS always do well in inflationary environments, but that is not always true in the short term.

If real yields rise sharply, TIPS prices can fall — sometimes meaningfully.

C. Inflation protection is not the same as price stability

TIPS are designed to protect purchasing power over time, but they can still be volatile in the market. That makes them effective as a long-term inflation hedge, but not necessarily a short-term “safe” asset in every environment.

D. Tax complexity in taxable accounts

TIPS can generate “phantom income” because investors may owe taxes on inflation adjustments to principal even before maturity. That makes them especially attractive in:

- IRAs

- Roth IRAs

- Other tax-advantaged accounts

For many retirees, placement matters almost as much as allocation.

Phantom Income: Occurs when the IRS requires that you pay taxes on income you have not physically received. This is usually seen in businesses and investments and is a mismatch between your tax liability and your actual cash flow. A paper gain without actual cash going into your bank.

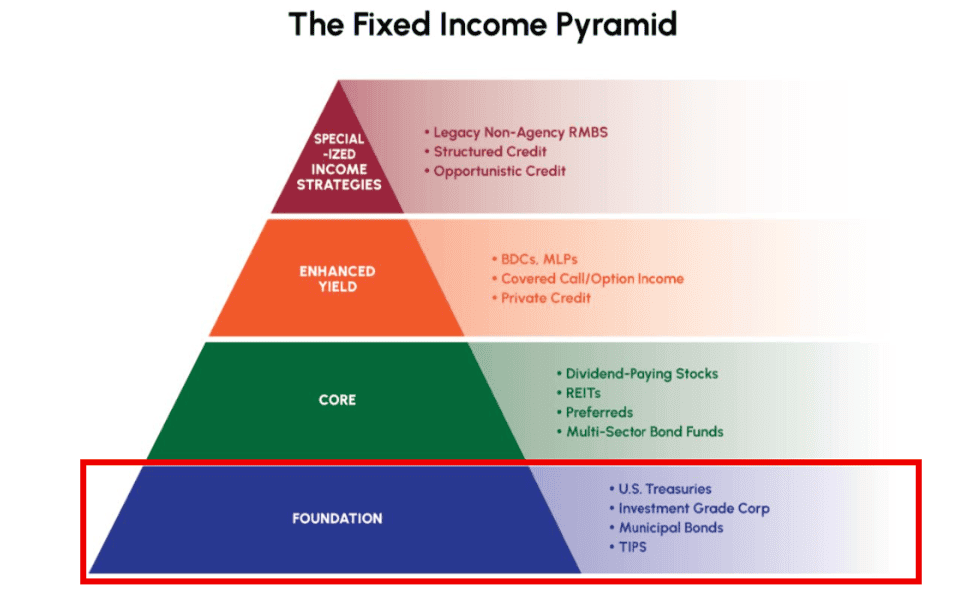

5. Where TIPS Fit in a Retirement Income Portfolio

In a retirement income pyramid, TIPS belong in the foundation. They are not there to maximize yield. They are there to help provide:

- High-quality bond exposure

- Inflation protection

- Stability of purchasing power

- Diversification against nominal bond risk

That makes them a natural complement to other foundational assets such as:

- U.S. Treasuries

- Investment-grade corporate bonds

- Municipal bonds (for taxable investors)

- Agency mortgage-backed securities

A retiree might think of TIPS as the portion of the portfolio designed to answer this question:

“What part of my income strategy is specifically built to defend against inflation?”

That is a different job than the one performed by corporate bonds or dividend stocks. And that is precisely why TIPS can deserve a dedicated place in the portfolio.

6. How Much a Retiree Might Own

TIPS are usually not an all-or-nothing allocation. Instead, they are often used as a targeted sleeve within the foundational fixed-income allocation. A general framework might look like this:

Conservative retiree

10%–25% of the fixed-income allocation. If you have a $1 million dollar portfolio – that would represent $100,000 to $250,000 in TIPS

Moderate retiree

5%–15% of the fixed-income allocation. In that same $1 million dollar portfolio – that means $50,000 to $150,000 in TIPS.

Income-maximizing retiree

0%–10% of the fixed-income allocation. In a $1.0 million dollar portfolio this is a maximum of $100,000 in TIPS.

The right amount depends on several factors:

- Inflation sensitivity of living expenses

- Other guaranteed income sources (Social Security, pension, annuity)

- Need for current income versus future purchasing power

- Overall bond allocation

- Risk tolerance

The key is not whether a retiree should own only TIPS. The key is whether they should own some TIPS. For many retirees, the answer is yes.

7. Bottom Line

TIPS are not flashy. They do not usually lead the league in yield. They rarely generate excitement. And in periods when inflation is calm, they can feel unnecessary. But retirement income investing is not about excitement. It is about solving problems before they become painful. And one of the biggest long-term problems retirees face is inflation quietly eroding spending power.

That is why TIPS can play such a valuable role as a foundational retirement income asset. They offer:

- Government-backed credit quality

- Explicit inflation protection

- Useful fixed-income diversification

- A way to defend real purchasing power over time

For retirees building a durable income portfolio, TIPS may not be the star of the show. But they can be one of the reasons the plan still works 10 or 20 years from now.

You can purchase directly from the government website here: TIPS — TreasuryDirect

Disclaimer: This Blog Post is for general information and entertainment purposes only. Readers are encouraged to consult with qualified professionals before making decisions based on the content provided. We are not responsible for any losses, damages or inconveniences caused by the use of this blog content.