Are you feeling uneasy with the volatility in today’s stock market? If so, you’re not alone. Many retirees and near-retirees are wondering how to protect their hard-earned savings while still participating in market growth. Navigating market volatility in retirement can be challenging, but looking at history may provide insights on how to navigate these uncertain times.

History Lesson: The Rise and Fall of Market Champions

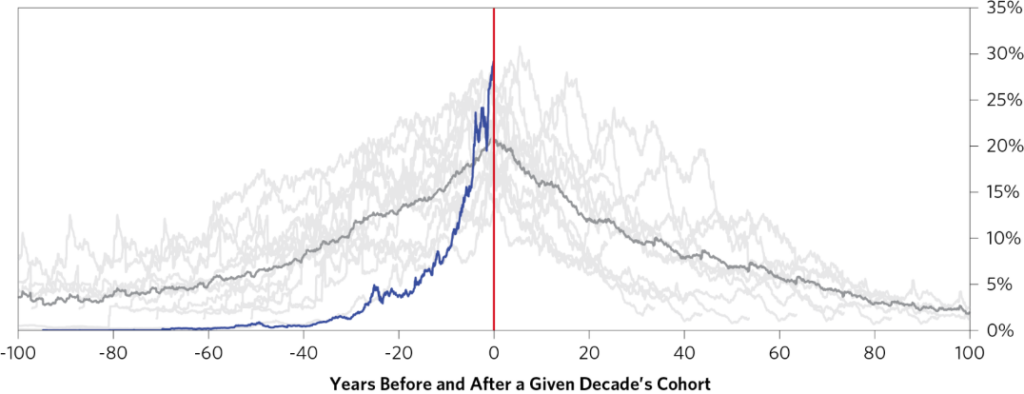

History tells us that dominant companies don’t stay on top forever. According to Barron’s, the “Magnificent Seven” stocks (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla) fueled more than half of the S&P 500’s 23% gain in 2024 as they soared an average of 60%. But fast forward to March 2025, and they’re down an average of 15%, accounting for about 95% of the index’s 6% decline. Are they still the Magnificent Seven—or the Lagging Seven?

This level of market concentration is concerning but not unprecedented. Looking back 120 years, we see a repeating cycle:

- Railroads once dominated – At their peak, railroads made up over one-third of the stock market, only to decline as new industries emerged.

- Big Oil took over – Exxon, Chevron, and others became the market’s heavyweights, but over time, new energy sources and tech disrupted their dominance.

- Tech and AI are today’s leaders – Will they follow the same fate? History suggests that even the biggest players struggle to maintain their edge forever.

As hedge fund manager Bridgewater Associates notes in The Life Cycle of Market Champions: “

“Throughout history, certain companies have dominated the equity market, but the process of creative destruction makes staying on top for long periods of time very difficult.”

For retirees, this is an essential lesson. If history repeats itself, relying too heavily on today’s market darlings can be a risky game.

What does this mean for Retirees?

If you’re retired or close to it, these market cycles make three things very clear:

- No company or sector dominates forever – Even the strongest businesses face disruption, regulation, and changing consumer trends.

- It’s likely too late in the game to swing for the fences – Younger investors can afford to take big risks, but retirees should prioritize protecting their nest egg.

- You need a plan to manage downside risk and volatility – The key to long-term financial security is balancing risk and reward. As the saying goes, “Pigs get fat, Hogs get slaughtered.”

How to Protect Your Retirement Portfolio

Here are three steps you can take to safeguard your savings in today’s unpredictable market:

1. Diversify Beyond the “Hot Stocks”

If too much of your portfolio is concentrated in a few big tech names, consider broadening your exposure. Make sure to ask your financial advisor to look at your overall exposure to the Mag Seven over your entire portfolio of funds. Consider more:

- Dividend-paying stocks – These can provide steady income even when markets are choppy.

- Bonds and fixed income – A mix of Treasury bonds, municipal bonds, and high-quality corporate bonds can offer stability. See my Post on Investing in Treasury Bonds.

- Alternative investments – Real estate investment trusts (REITs), commodities, and infrastructure investments can help hedge against stock market volatility.

2. Focus on Income and Capital Preservation

When you were working, your primary goal was to grow your savings. In retirement, it’s about making sure your money lasts. Are you ready for retirement?

- A well-structured withdrawal plan – The 4% rule is a starting point, but retirees should adjust based on market conditions.

- Bucket strategy – Keeping 3-5 years of living expenses in cash or conservative investments can help you avoid selling stocks during downturns. Setting up a bond ladder can help with this.

- Annuities or other income streams – These can provide guaranteed income, reducing reliance on market returns. This may include taking social security earlier than 70.

3. Rebalance and Manage Risk Regularly

It’s easy to get caught up in the hype of certain stocks or trends, but regular portfolio reviews with your financial advisor are crucial. Consider:

- Annual rebalancing – Adjusting your portfolio to maintain your target asset allocation.

- Risk assessment – As you age, you may want to shift toward a more conservative portfolio.

- Tax efficiency – Managing withdrawals in a tax-smart way can help you keep more of your money.

Final Thoughts

Market volatility is a fact of life, but history shows us that no stock or sector stays dominant forever. As a retiree, your priority should be protecting your wealth while still allowing for growth. By diversifying, focusing on income, and actively managing risk, you can navigate market uncertainty with confidence.

Disclaimer: The information in this blog post is for educational and informational purposes only and should NOT be construed as financial or investment advice. Investing carries risks, including the loss of principal. Always conduct your own research and consider consulting with a qualified financial professional before making any investment decisions.

This post was written with the help of my husband, a FINRA registered rep.