Dr. Hendrik Bessembinder, a Professor of Finance at Arizona State University’s W.P. Carey School of Business, conducted a groundbreaking study that challenges common investing assumptions—especially for those nearing or in retirement. His 2018 paper, “Do Stocks Outperform Treasury Bills?“, sheds light on a surprising truth: most individual stocks do not generate market-beating returns.

📖 Source: Read the full study here (also below)

The Study: A Deep Dive into Market Returns

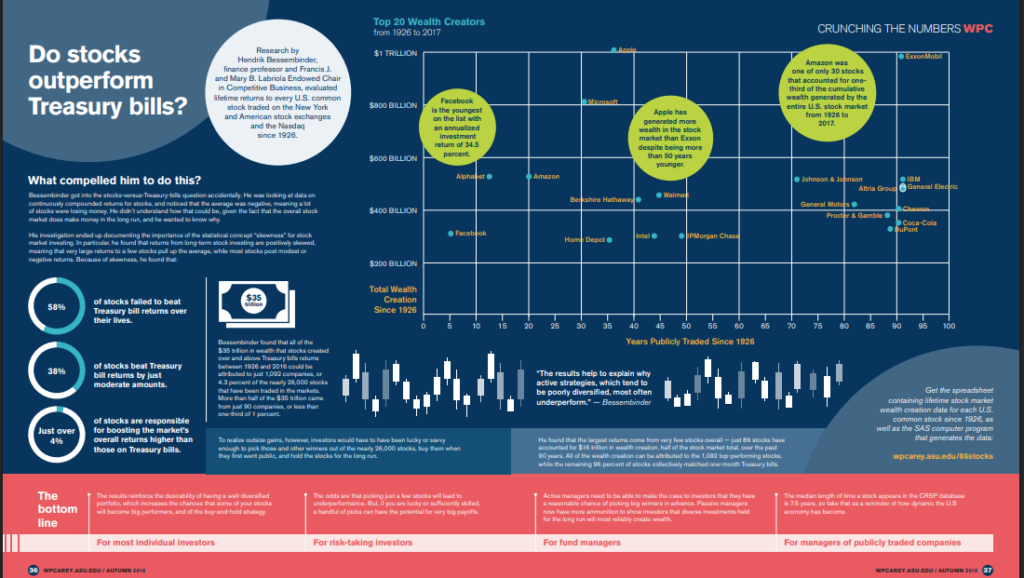

Bessembinder analyzed over 26,000 individual stocks in the Center for Research in Security Prices (CRSP) database, dating back to 1926. His findings were eye-opening:

✅ All $35 trillion in net stock market wealth creation from 1926 to 2016 came from just 1,092 companies—a mere 4.3% of stocks that have ever traded.

✅ When reviewing the compounded returns of all stocks, only 43% (three out of seven) outperformed one-month U.S. Treasury bills over their lifetime. That means 57% of stocks failed to beat Treasuries.

Key Takeaways for Investors Over 60

🔹 Most Stocks Underperform: The majority of stocks deliver lower returns than Treasury bills, making stock-picking a risky game.

🔹 The Market is Extremely Skewed: A tiny fraction of stocks (around 4%) drive nearly all long-term market gains. If you don’t own those winners, your portfolio may significantly underperform.

🔹 High Failure Rate: Many companies see long-term declines or even go to zero. Holding just a few stocks increases the risk of being on the wrong side of the odds.

🔹 The “Magnificent 7” Stocks Dominate Today—But for How Long?

Currently, Apple, Microsoft, Nvidia, Amazon, Alphabet (Google), Meta, and Tesla—known as the “Magnificent 7”—have driven a large portion of recent market gains. These stocks are heavily weighted in major index funds, meaning many investors own them multiple times through different funds.

However, history shows that market leadership doesn’t last forever. Railroads once dominated the market, followed by oil giants, and later tech companies. While these companies may still perform well, investors should be mindful of their concentration risk. If the Magnificent 7 stumble, many portfolios—especially those relying heavily on index funds—could take a significant hit.

🔹 What This Means for You: If you’re retired or approaching retirement, relying on individual stock-picking is not a reliable strategy. Instead, diversification and principal protection can help you move into retirement with more confidence. That said, it’s also wise to review your portfolio to ensure you’re not overly exposed to the Magnificent 7, as their dominance could fade over time.

Final Thoughts

Bessembinder’s research challenges traditional stock market wisdom. As you consider or move into the retirement phase of life, protecting your portfolio from unnecessary risk or draw down risk is critical. Make sure you have regular meetings with your financial advisor (Read: Choosing a Financial Advisor) or continue to monitor your portfolio regularly.

Disclaimer: The information in this blog post is for educational and informational purposes only and should NOT be construed as financial or investment advice. Investing carries risks, including the loss of principal. Always conduct your own research and consider consulting with a qualified financial professional before making any investment decisions.