Two updates matter right now. First, SECURE 2.0, signed in late 2022, changes catch-up rules and adds a Roth requirement for high earners. Second, a recent executive order is allowing people to add more alternative assets to their 401(k)s. More choice can sound good, but it brings new risks.

1. SECURE 2.0: 2025 Catch-ups and 2026 Limitations

In the past, you could contribute a set amount to your 401(k) pre-tax. If you were 50 or older, you could also make catch-up contributions. Key points to keep in mind:

- In 2024 & 2025, the standard 401(k) employee contribution limit is $23,000.

- If you are age 50 or older, you can add a $7,500 catch-up. That brings your total to $30,500.

- All of that could be pre-tax under current rules.

Starting in 2025, people ages 60 to 63 can make a “super catch-up.” Instead of the usual $7,500 catch-up, you can put in up to 150 percent of that amount. Using today’s numbers, that is an extra $11,250. (See Blog Post New Retirement Rules for 2025)

Translation: If you are 60 to 63 in 2025, your total potential contribution could reach $34,250, based on current limits.

Starting in 2026, if your wages from your employer are more than $145,000, your catch-up contributions must go to the Roth side of the 401(k), not the pre-tax side.

What that means:

- No upfront tax deduction on your catch-up dollars.

- You may be adding to your 401(k) at your highest tax rate. Talk with your tax professional to see if that tradeoff makes sense for you.

- Another path is to make pre-tax contributions on what you can now, then consider Roth conversions later, when your tax bracket may be lower.

- If your employer plan does not include a Roth option when the new rule starts, catch-up contributions may not be allowed for affected high earners. Check with HR or your plan administrator now.

Why this matters for high earners

- Tax planning shifts. The Roth requirement pushes taxes forward on catchups. For many people at peak income, that is a tough pill. A staged Roth conversion in lower-income years may be more tax efficient. Be sure to discuss with your financial planner and accountant.

- Retirement income mix. Roth dollars can help you manage taxable income in retirement. Flexibility later is valuable.

- Timing. The age 60 to 63 “super catch-up” lasts only four years. If you plan to use it, map out those years now.

- Employer readiness. Some plans are still adding Roth features and updating systems before 2026.

Bottom Line

SECURE 2.0 helps late savers at ages 60 to 63, but it also shifts high-earner catch-ups to Roth starting in 2026. The policy goals are clear, yet the best move for you depends on income, taxes, and timing. Thoughtful planning helps ensure you keep more of what you’ve earned.

2. Alternative Investments for your 401K? Maybe….

President Trump issued an executive order on September 7, 2025, directing the Labor Department to allow holders of 401(k) and other defined-contribution retirement plans to invest in alternative assets. These include private equity, real estate and digital assets such as bitcoin. While this might allow higher returns, are the risks worth the reward?

Retirement should be a time to simplify, not complicate. Advisors might pitch these alternative investments as a smart way to diversify your portfolio and boost your yield. But, with Halloween on the horizon – Buyer Beware! Here’s the reality: these investments carry risks that can jeopardize the very thing retirees need most — stability, liquidity, and dependable income. As a retiree, you don’t have time on your side to recoup losses.

Two articles you might find interesting about these Alternative Investments:

My Hard-Knock Lesson in Private Investing – by Daniel P Wiener, Barron’s / Other Voices, Sep. 29

Credit Markets Are Hot, But Froth is Worry – by Matt Wirz & Sam Goldfarb, Wall St. Journal, Sep. 29

The Hidden Dangers of Alternatives

Alternative investments — think private equity, hedge funds, real estate partnerships, or private credit funds. These are often sold as exclusive opportunities that can “smooth returns” or “outperform stocks and bonds.” But what’s left out of the glossy brochures is just as important:

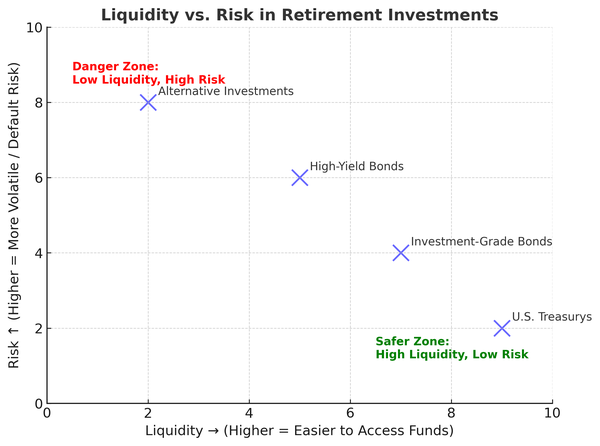

- Illiquidity: Your money may be tied up for 5, 7, or even 10 years. That’s fine if you’re 40. But when you’re retired, flexibility matters.

- Unpredictable Returns: Promised double-digit gains often take much longer than expected — and sometimes never show up at all.

- Opacity & Tax Complexity: Unlike a simple dividend-paying stock or municipal bond, these funds often provide limited reporting, delayed tax documents, and complicated rules that can shrink your net return.

- Accredited Investor: Often these investments require you to have net worth of over $1.0 million and a minimum annual income of $200,000 ($300,000 with spouse).

What’s Bubbling in the Credit Markets

Corporate debt is another area demanding caution. After years of cheap money, companies that borrowed heavily are starting to show cracks:

- Low Risk Compensation: Both investment-grade and high-yield bonds offer only a thin yield premium compared with U.S. Treasurys. In other words, you’re taking on more risk without much extra reward.

- Rising Defaults: Private credit and leveraged loan markets are seeing more missed payments, with some companies resorting to IOU-style “payment-in-kind” interest.

- Market Sensitivity: Even a single bankruptcy or fraud case can send shockwaves through bond markets.

As the Wall Street Journal recently noted, the credit market may be “hot,” but the froth carries worry.

The Retirement Bottom Line

For retirees, investing is no longer about swinging for the fences. It’s about protecting income and principal. That means:

- Prioritize Liquidity → Keep at least one year (or more) in fairly liquid assets to live on so .

- Diversify with Purpose → Don’t overload on any one risky category just because it’s trendy.

- Focus on Predictable Income → Steady bond ladders, dividend-paying stocks, and conservative funds often do more for peace of mind than exotic alternatives.

Alternative investments and corporate debt aren’t always bad — but they aren’t always right for retirement portfolios either. The key is asking: Does this investment align with my need for safety, stability, and sleep-at-night income?

The below chart is a visual of the risks of different types of investments.

If you enjoyed this post, subscribe below for more!

Disclaimer: The information provided in this post is for general informational purposes only and does not constitute financial, investment, tax, or legal advice. While we strive to provide accurate and up-to-date information, we make no warranties or guarantees regarding its accuracy or completeness. Always consult with a qualified financial advisor, tax professional, or legal professional before making any financial decisions. Any reliance you place on the information in this post is strictly at your own risk.