In 2022, after my husband sold half of his company, our financial advisor placed part of our savings into a laddered municipal bond portfolio. The goal was simple: create a steady stream of income in retirement.

Not long after, Russia invaded Ukraine, and the Federal Reserve raised interest rates by four full percentage points (4.0%) in a single year. Suddenly, our bond portfolio dropped significantly in value—and it has yet to recover.

Bonds are supposed to be safe, right? So why was I staring at these “paper” losses, and when would they come back?

That experience pushed me back to my professional roots in finance to revisit what bonds can and can’t do—and more importantly, what went wrong with our portfolio.

The General Benefits of Bonds

When built correctly, a laddered bond portfolio is one of the most reliable strategies for generating steady, predictable income in retirement. Municipal bonds, in particular, are attractive because they combine safety with valuable tax advantages. Historically, their default rates are extremely low—about 0.05% for A-rated bonds and essentially zero for AAA-rated bonds.

The beauty of individual bonds is that if you hold them until maturity, you not only collect interest along the way but also almost always receive your full principal back.

Bond funds, however, behave more like stocks. The bonds inside them are bought and sold daily, which makes their market value fluctuate. If you need to sell shares during a downturn, you may end up locking in a loss.

A laddered bond portfolio helps smooth those risks by staggering maturities—monthly, quarterly, or annually—so you always have income coming due. While it may not offer the upside potential of bond funds in a rising market, a properly structured ladder delivers predictability and stability—exactly what most retirees want.

Where My Advisor Went Wrong

Financial advisors hold professional licenses, but passing those exams only gets you in the door. It takes years of experience to truly understand the bond market. I know this firsthand—I once held my Series 7, 63, and 24 licenses and spent decades helping municipalities issue bonds.

The U.S. bond market is massive—about $57 trillion outstanding compared with $46 trillion in the stock market. That makes it roughly 23% larger than equities, and far more complex than most people realize. Beyond interest rate risk, there’s bond pricing, yield to maturity, yield to call, duration, and credit. Many advisors lean heavily on stock funds and bond funds because they’re easier to manage and often more profitable. Structuring a proper ladder of individual bonds takes time, attention, and specialized knowledge.

In our case, the problem wasn’t that we owned bonds—it was that our advisor created a sloppy, unstructured ladder that didn’t fit our needs. That mistake left us exposed to risks we didn’t even realize we had.

And we’re not alone. When we began helping both my mother and my husband’s 88-year-old uncle, we discovered their portfolios were also poorly structured. I suspect that’s partly because well-designed laddered bond portfolios take a lot of time and don’t generate much revenue for the advisor.

Check out my Blog Post “Investing for Aging Parents: Practical Tips“

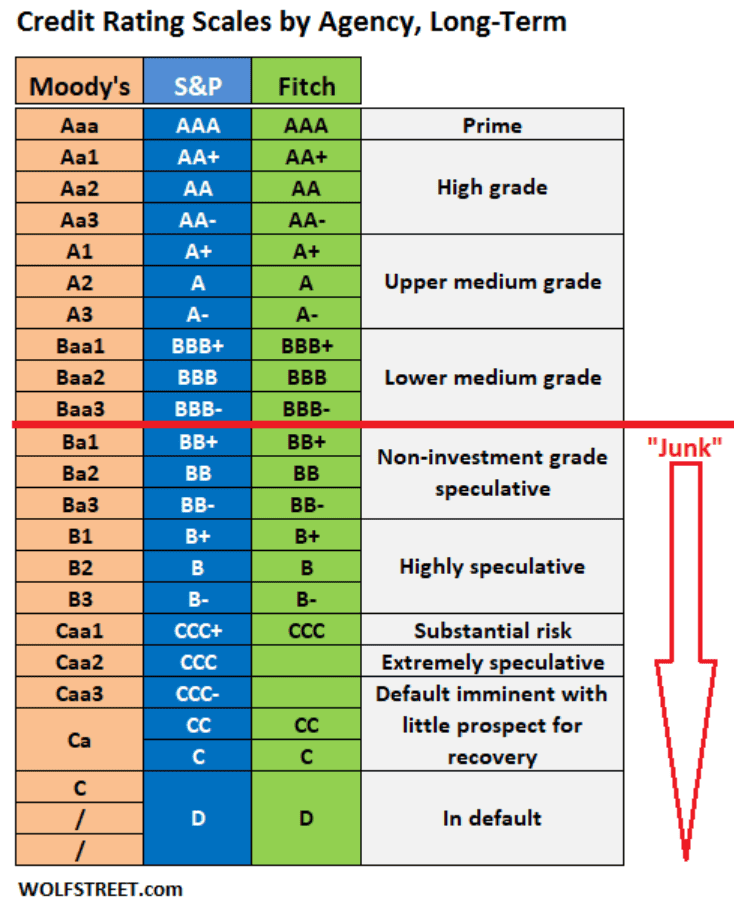

Understanding Credit Risk

Credit quality is one of the first things to evaluate in any bond portfolio. Municipal bonds with ratings of A or higher carry extremely low default risk, but even within that safe zone, there are important differences.

- General Obligation (GO) Bonds: Backed by the full faith and credit of the issuing municipality, secured by its authority to levy unlimited property taxes. This makes them the strongest form of municipal debt.

- Revenue Bonds: Secured by specific revenue streams—such as water fees, tolls, or utility charges. Because these revenues depend on demand and economic conditions, revenue bonds generally carry more repayment risk.

Both types can hold the same credit rating, but when you read the fine print in the official statement, revenue bonds usually have more risk than GO bonds.

Most advisors don’t dig into these details. I had an advantage from my 25 years in commercial and investment banking, where credit analysis was second nature. Without that background, many investors—and even some advisors—don’t fully appreciate the differences.

Below is the Credit Rating Scales by Agency.

The Bigger Issue: Duration Risk

Another key factor is duration risk—the sensitivity of a bond’s price to changes in interest rates. The longer the maturity, the more its price rises or falls when rates move.

- If rates rise, long-term bonds lose more value than short-term bonds.

- A bond with a 10-year duration will typically lose about 10% of its value if interest rates rise by 1%.

- Keeping maturities shorter or using a laddered portfolio helps reduce this risk.

Unfortunately, in our case, our advisor bought bonds maturing in 2049—more than 25 years out. That long duration created unnecessary risk. So when interest rates spiked in 2022, our portfolio showed significant paper losses.

It’s important to note: those losses weren’t realized because we didn’t sell. If held to maturity, the bonds will still pay out. But in the meantime, the portfolio looked far weaker on paper.

What We Should Have Done Better

Part of the problem rests with us. We gave our advisor discretion to make investment decisions without requiring our approval. We trusted him, but we didn’t hold him accountable. At the time, my husband was focused on his company, and I was working as a CFO of a school district. We didn’t ask the right questions or set clear boundaries.

Looking back, we should have:

- Set specific limits on how far out we were comfortable laddering maturities.

- Reviewed the ladder structure carefully instead of assuming it was handled correctly.

- Required our advisor to confirm key decisions before executing them.

He didn’t, and we fired him.

The Lesson

Even with “safe” investments like municipal bonds, you must know what you own and how it’s structured. Bonds can absolutely deliver stability and income in retirement—but only if the portfolio matches your goals, your time horizon, and your comfort with risk. Now I am truly hoping for Federal Chairman Powell to begin to lower interest rates, so my bond portfolio might begin to recover.

Closing Thought

If you’re holding bonds today, ask yourself: Do I know how my ladder is structured? Am I truly comfortable with the maturities, risks, and income streams I’ve committed to? These aren’t just technical details—they’re the difference between sleeping well at night and worrying through every rate hike. The safest investment is the one you understand completely.

Disclaimer: The information provided in this post is for general informational purposes only and does not constitute financial, investment, tax, or legal advice. While we strive to provide accurate and up-to-date information, we make no warranties or guarantees regarding its accuracy or completeness. Always consult with a qualified financial advisor, tax professional, or legal professional before making any financial decisions. Any reliance you place on the information in this post is strictly at your own risk.