A Personal Note Before We Begin

For nearly two decades, I sat on the other side of the table — helping municipalities, school districts, and park districts borrow money through the bond market. I watched how the sausage gets made. And what I learned from all those years in the business changed the way I think about retirement income.

Here’s the distinction that matters most and that too few investors make: it’s not how much income you’ll have in retirement. It’s how much you’ll actually keep.

Most people chasing yield focus on the number they see — the interest rate, the coupon, the payout. What they miss is what happens after taxes take their cut. I’ve seen investors lock in impressive-looking yields only to watch a meaningful slice quietly disappear to the government before it ever reaches their pocket.

That’s where municipal bonds come in. They’re not flashy. They don’t make headlines. But for higher tax bracket investors, they do something no other bond can claim: they routinely put more money in your pocket on an after-tax basis than higher-yielding alternatives.

That’s the foundation.

So What Exactly Are Municipal Bonds?

Municipal bonds — “munis,” if you want to sound like someone who’s spent too many hours in bond markets — are issued by state and local governments to finance public projects. Schools, roads, water systems, bridges. The stuff that holds a community together.

In exchange for lending them your money, you receive regular interest payments and your principal back at maturity. Simple.

But here’s what makes them different from every other bond in your portfolio: the interest is typically exempt from federal income taxes, and often from state and local taxes too. That’s not a loophole. It’s by design — it’s how governments attract investors to fund public infrastructure without paying corporate-level rates.

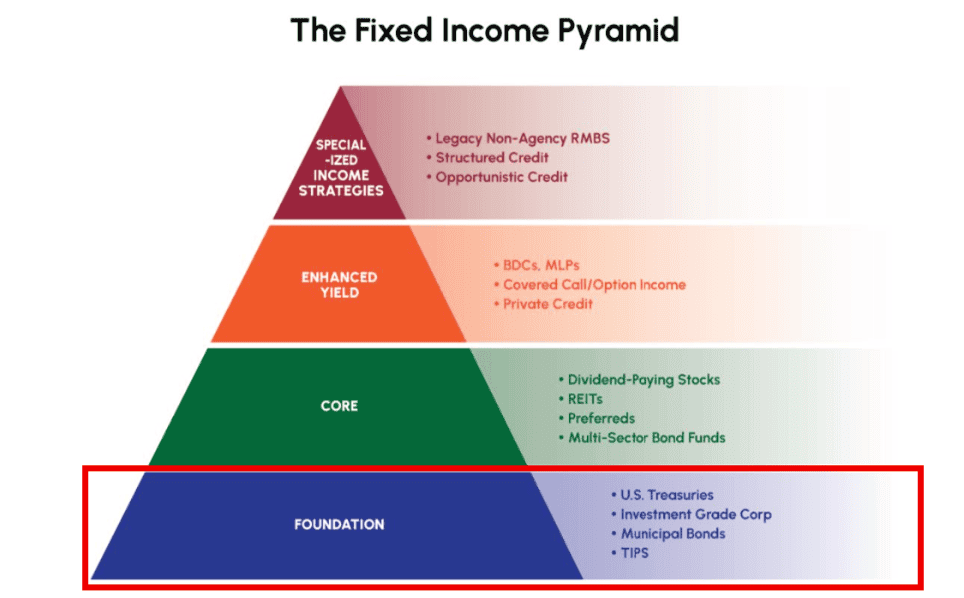

Why I Think of Munis as a Foundation Asset — Not an Add-On

If you have been following our series on foundational income, municipal bonds are not a supporting player — they are a foundational building block, particularly for higher income investors.

They combine:

- High-quality credit exposure

- Predictable cash flows

- Embedded tax efficiency

While other assets may offer higher nominal yields, munis are designed to deliver more tax efficient income — income that investors actually keep.

The Math That Changes How to Think About Yield

Municipal bonds are best understood through the lens of after-tax yield, not stated yield.

Tax-Equivalent Yield = Municipal Yield ÷ (1 − Tax Rate)

For higher-income retirees, this math is powerful. A 3–4% municipal yield can translate into a meaningfully higher taxable equivalent yield.

Example: Assume you are in the 30% tax bracket. You have a muni bond paying a 3.5% coupon. Your taxable equivalent yield would be 5.0% (3.5% ÷ (1.0 − 0.30)).

The benefit compounds over time through reduced tax drag. This makes munis especially effective for:

- Taxable accounts

- Income-focused withdrawal strategies

- Investors managing bracket sensitivity in retirement

A Word on Risk — Because I Won’t Pretend There Isn’t Any

Municipal bonds have historically exhibited strong credit characteristics, particularly in the investment-grade segment:

- Default rates are low relative to corporate bonds. Defaults on investment grade municipal bonds run about 0.10% over a 10-year period, compared to 2.2% for investment-grade corporate bonds.

- Issuers have strong incentives to maintain market access.

- Many bonds are backed by a tax levy — unlimited — requiring bondholders to get paid before anyone else.

However, municipal bonds are not risk-free. Low default rates are not zero default rates. A few things are worth watching:

The pension obligations that many state and local governments are carrying are significant — and some jurisdictions are managing them better than others. Budget discipline matters. And certain types of munis — particularly revenue bonds tied to specific projects like hospitals or toll roads — carry more targeted risk than general obligation bonds backed by a government’s taxing authority.

The practical implication: quality and diversification matter more than squeezing out extra yield. If a muni fund or individual bond is offering a yield that seems too good compared to its peers, there’s usually a reason.

Structure Matters

Not all munis are alike, and a basic distinction will serve you well.

General obligation bonds are backed by the taxing authority of the issuing government — the full faith and credit of a state or municipality. These tend to anchor the highest-quality end of a muni allocation.

Revenue bonds are backed by cash flows from a specific project — a toll road, a hospital system, a water utility. They typically offer a bit more yield in exchange for more targeted risk.

A thoughtful portfolio usually holds a blend of both. The GO bonds provide stability; the revenue bonds add a little income without reaching too far up the risk ladder.

Muni Bond Funds vs. Individual Bonds: Why I Prefer the Ladder

When most people think about adding municipal bonds to their portfolio, they reach for a fund — a muni ETF or mutual fund that bundles hundreds of bonds together. It feels diversified. It feels easy. And honestly, the financial industry has done a great job marketing it that way.

But here’s what the fund brochure doesn’t highlight: a muni bond fund behaves a lot more like a stock fund than most investors expect.

The Problem with Funds

When you own a muni bond fund, you don’t own bonds in the traditional sense. You own shares of a fund that owns bonds — and that distinction matters enormously in retirement.

Bond funds have no maturity date. The fund never “matures.” It just keeps rolling, buying and selling bonds continuously. That means:

- Your principal is never guaranteed to come back. If interest rates rise, the fund’s share price falls — and unlike an individual bond, there’s no maturity date where you get made whole.

- You have no control over what you own. The fund manager decides what to buy, sell, and hold. You’re along for the ride.

- Income can fluctuate. The yield isn’t fixed. As the fund’s holdings change, so does your payout.

For someone in accumulation mode, that volatility is manageable. For a retiree depending on that income? It introduces uncertainty you simply don’t need.

The Case for a Bond Ladder

A bond ladder is exactly what it sounds like: a portfolio of individual bonds with staggered maturity dates — say, bonds maturing every one to two years over a 10ish year horizon.

The beauty of a ladder is what it eliminates: uncertainty. Each bond in your ladder has a defined maturity date and a known coupon payment. You know what you’re getting paid, and you know when you’re getting your principal back. When a bond matures, you reinvest the proceeds at current rates — which is actually an advantage in a rising rate environment, not a liability.

What a ladder gives you that a fund never can:

- Certainty of income. Your coupon payments don’t change with the market.

- Return of principal. Barring default, you get your money back at maturity — full stop.

- Rate rise resilience. When rates go up, you reinvest maturing proceeds at higher yields rather than watching your fund’s NAV decline.

- No management fees eating into your tax-exempt income.

The Honest Tradeoff

Laddering individual munis requires more capital to do it well — you generally need at least $100,000 to $200,000 to build a properly diversified ladder, since munis are typically sold in $5,000 increments and you want exposure across issuers, states, and maturity dates.

If your muni allocation is smaller than that, a high-quality, low-cost muni ETF from a shop like Vanguard or Fidelity is a perfectly reasonable starting point. Just go in with eyes open: you’re accepting fund-like behavior, not bond-like behavior.

But for retirees with meaningful taxable account balances and a genuine need for predictable, tax-efficient income — a laddered portfolio of individual investment-grade munis is, in my view, the cleaner, more purposeful solution.

It’s the difference between a paycheck and a variable annuity. In retirement, I’ll take the paycheck every time.

How Much a Retiree Might Own

As a foundation asset, municipal bond exposure is often meaningful and intentional — not residual.

| Investor Type | Allocation | Profile |

| Conservative | 25–50% | Income-first, lower risk tolerance |

| Balanced | 15–35% | Growth + income, tax-conscious |

| Growth | 5–20% | Appreciation-focused, higher bracket |

Allocations tend to increase with higher marginal tax rates, larger taxable account balances, and greater emphasis on income efficiency.

What Munis Actually Do for Your Portfolio

I like to think of it this way. U.S. Treasuries give you safety. TIPS give you inflation protection. Municipal bonds give you something equally important: tax-aware income — income designed to maximize what you actually get to spend.

They reduce the drag between what your portfolio earns and what arrives in your checking account. They help dampen volatility in a way that lets you sleep at night. And they improve the quality of your income, not just the quantity.

That last point is the one I’d most want you to take away from this. In retirement, it’s not about chasing the biggest number on paper. It’s about keeping more of what you earn. Munis are built, from the ground up, to do exactly that.

Frequently Asked Questions

Are municipal bonds really safer than corporate bonds?

Investment-grade munis have historically defaulted at a rate of about 0.10% over ten years, compared to roughly 2.2% for investment-grade corporate bonds. They’re not risk-free — but their default track record is meaningfully stronger.

Do munis make sense if I’m in a lower tax bracket?

The tax benefit shrinks as your bracket shrinks. In lower brackets, the after-tax math often favors taxable bonds with higher nominal yields. This is why munis tend to make the most sense for investors in the 24% bracket and above.

Should I hold munis in my IRA or 401(k)?

Generally, no. The tax exemption is already wasted inside a tax-deferred account. Munis are most powerful in taxable brokerage accounts where their tax efficiency actually shows up in your pocket.

What’s the difference between a muni fund and individual bonds?

Individual bonds give you certainty — you know your yield and your maturity date. A bond ladder of individual munis provides predictable income and return of principal at each maturity, with no management fees. Funds offer diversification and liquidity but introduce interest rate risk and don’t have a fixed maturity — they behave more like a stock fund than most investors expect. For retirees with $100,000 or more to allocate, a laddered individual bond portfolio is typically the more efficient choice. Below that threshold, a low-cost muni ETF from a firm like Vanguard or Fidelity is a solid starting point.

How do I know if a muni is high quality?

Look for investment-grade ratings from Moody’s or S&P — anything rated Baa/BBB or above. General obligation bonds from financially stable states and municipalities tend to anchor the highest-quality end of any muni allocation. If a bond is offering a yield that looks unusually high compared to peers, dig in — there’s usually a reason.