The current financial markets have been volitale. On January 27, 2025, Nvidia stock dropped $600 billion in market value due to fears of the Chinese start-up DeepSeed.

If you are nearing retirement, this volatility can be nerve-wrecking. One of the areas that has been difficult for me to stomach is fixed income bonds. Two years ago, as I was retiring, my husband and I put a significant amount of money in a municipal bond ladder. Interest on those funds would replace my salary federally tax-free. As interest rates continued to rise, we have seen a large “paper” loss on those bonds. (Remember, you don’t take the loss on an investment unless you sell it.) Now we are looking for additional ways to improve that income without having to take the “paper” losses on our bond ladder portfolio. Here are three options we are considering all with varying risk;

- Taxable Fixed-Income Investments (Low Risk)

- Dividend Paying Mutual Funds (Moderate Risk)

- High-Yield Dividend Stocks (Moderate Risk)

1. Fixed-Income Investments for Stability (Low Risk)

For investors prioritizing safety, fixed-income securities such as bonds and Depository Trust Company (DTC) certificates of deposit (CDs) offer reliable interest income. Some key fixed-income options include:

- Treasury Bonds: U.S. Treasury bonds provide government-backed security. These bonds are federally and state taxable but have higher yields than municipal bonds. As of this writing, 10-year Treasury Bonds are yielding 4.47%.

- Corporate Bonds: Investment-grade corporate bonds from financially stable companies yield higher interest than government securities while maintaining a relatively low risk profile. Based on credit quality, yields on corporate bonds range from 4.78% (AAA-rated) to 5.89% (A-rated)

- High-Yield Savings Accounts & CDs: These offer safe, predictable returns with FDIC insurance, making them a suitable choice for capital preservation and modest income generation. 10-Year DTC CDs are yielding 5.10%. Not bad for safe returns.

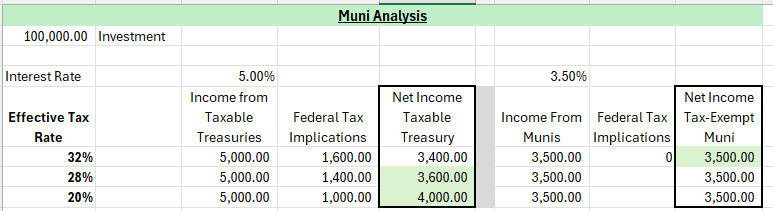

- Municipal Bonds: Municipal bonds are issued by state and local government agencies. They have varying credit quality from A to AAA. I prefer to invest in at least AA (S & P) or Aa (Moody’s) rated bonds or better. Only invest in municipal bonds if your tax bracket is greater than 28% otherwise you are losing potential income. (See chart below for effective-tax breakeven points for municipal bonds)

2. Mutual Funds with Strong Dividend Payouts (Moderate Risk)

We decided to add some mutual funds that focus on dividend-paying stocks to add diversification to our portfolio while also generating consistent income. Some of these options include:

- Dividend Growth Funds: These funds invest in companies with a strong track record of increasing their dividends over time.

- High-Yield Equity Income Funds: These funds target stocks with above-average dividend yields, balancing risk and reward.

- Balanced Funds: These funds combine dividend-paying stocks with fixed-income assets, providing both income and stability.

Example Ranges of Income

- Conservative Dividend Funds (1.5% – 3% yield) – Focus on stable, blue-chip companies (e.g., Vanguard Dividend Growth Fund).

- Moderate Dividend Funds (3% – 4.5% yield) – Invest in a mix of high-yield and growth-oriented dividend stocks.

- High-Yield Dividend Funds (4.5% – 6%+ yield) – Often include REITs, energy stocks, or international dividend-paying companies, but may carry more risk.

Mutual funds have the advantage of professional management and diversification. This reduces the risk of relying on individual stocks for dividend income. While you are adding more risk to the portfolio by adding dividend paying mutual funds, you gain upside growth potential if the NAV (Net Asset Value) rises with the market.

Please consult a financial advisor or investment professional to help you select the best funds to meet your risk tolerance and financial income needs. This blog is for informational/entertainment purposes only.

If you need help finding a financial professional, consider reading my blog on selecting a financial advisor.

3. Investing in High-Yield Dividend Stocks (Moderate Risk)

Dividend-paying stocks, particularly those with a history of increasing payouts, can provide a steady stream of income while offering the potential for capital appreciation. Companies in sectors such as utilities, consumer staples, and healthcare often provide dividends. Some considerations when investing in dividend stocks include:

- Dividend Aristocrats: These are companies that have consistently increased their dividends for at least 25 consecutive years, such as Johnson & Johnson or Procter & Gamble.

- High-Yield Stocks: Companies with above-average dividend yields, such as REITs (Real Estate Investment Trusts) and energy infrastructure firms, can offer more significant payouts but often come with higher volatility.

- Dividend Reinvestment Plans (DRIPs): These allow investors to automatically reinvest dividends into additional shares, compounding their income over time.

While dividend stocks can provide attractive yields, it’s essential to assess the financial health of the company. Again, please consult with your financial professional to determine the best options for your portfolio.

Final Thoughts

We decided to add dividend paying mutual funds to boost our income with moderate risk. We like the fact that the mutual funds provide upside potential if the stock market continues rise. Additionally, we decided to start to sell some of our municipal bonds due to a change in our tax bracket and invest in Treasuries and DTC certificates of deposit. By making these two minor changes to portions of our portfolio we increased our annual income by almost 8%. Talk to your financial professional and see if there are ways you can increase your income. Learn how much you need to retire using Schwab’s calculator here.

Disclaimer: The information in this blog post is for educational and informational purposes only and should not be construed as financial or investment advice. Investing carries risks, including the loss of principal. Always conduct your own research and consider consulting with a qualified financial professional before making any investment decisions.

Before making any investment decisions, consider your risk tolerance and financial objectives, and consult with a financial professional if needed. By strategically selecting income-generating investments, you can work toward financial security and long-term wealth accumulation.