The Medicare Surprise Nobody Warned Us About

There’s one genuinely exciting thing about turning 65 — and no, it’s not your bathroom habits. You can finally apply for Medicare. After years of astronomical premiums, you’re ready for something more manageable, with coverage you can actually count on. Then, someone mentions IRMAA, and you think — who is this woman, and why does everyone keep bringing her up? Surely it won’t apply to you. But here’s the thing: IRMAA surprises most retirees. Without preparation, she will drain savings you spent a lifetime building.

This is the first in a four-part series on the hidden costs of retirement. Today: Medicare premiums in 2026 — and trust me, this one caught us completely off guard.

We Thought We Knew What to Expect

When my husband recently began the process of applying for Medicare, I assumed it would be fairly straightforward. We’d done our homework — or so we thought. What we discovered was a system far more complex than either of us had anticipated, with costs that vary significantly depending on something most people don’t think to ask about: your income from two years ago.

That single detail changed our entire outlook on retirement healthcare costs at a time when our primary work income was coming to an end.

How Medicare Actually Works: The Four Parts You Need to Know

Let’s start with the basics, because they matter more than people realize.

Medicare is the federal health insurance program for people 65 and older. It’s divided into several parts, each covering different things – and you need to understand all of them to avoid being caught short.

Medicare Part A covers hospital stays, skilled nursing facility care, hospice, and some home health services. For most people, Part A is premium-free — as long as you (or your spouse) worked at least 10 years and paid Medicare taxes. This is the good news.

Medicare Part B covers outpatient care — doctor visits, preventive services, lab work, and medical equipment. The base premium is $202.90 per month in 2026, but as you’ll see, that number can climb significantly depending on your income. Part B only covers 80% of approved costs, leaving you responsible for the remaining 20% — with no out-of-pocket maximum. That gap needs to be covered separately.

Medicare Part D covers prescription drugs. This is a separate plan you select, and costs vary widely depending on the medications you take.

Medigap or Medicare Advantage (Part C) exists specifically to cover that 20% that Part B leaves behind. Most people choose either a Medicare Supplement Insurance plan (Medigap) or a Medicare Advantage plan, which bundles Parts A, B, and often D into a single plan through a private insurer. Medigap plans offer more flexibility in choosing doctors; Medicare Advantage plans often have lower premiums but more restricted networks. Choosing between them deserves careful research.

Your total monthly healthcare cost in retirement will look something like this (Part A is not included because the cost is $0 for most people):

Part B premium + Part D premium + Medigap or Medicare Advantage = Your Real Healthcare Cost

What Medicare Doesn’t Cover: Dental and Vision

Perhaps the most universally frustrating gap — traditional Medicare does not cover routine dental or vision care. If you had employer-sponsored health insurance that included these benefits, you’ll now need to budget for them separately, either through standalone plans or out of pocket. For many retirees this comes as a genuine shock, especially after decades of comprehensive employer coverage.

When to Sign Up – and Why Timing Matters

If you’re already receiving Social Security benefits (or Railroad Retirement Board benefits), you’ll be automatically enrolled in Medicare Parts A and B starting the first day of the month you turn 65. Easy enough.

But if you’re like my husband — not yet taking Social Security, because we’re working on a spousal benefit strategy — you have to sign up on your own. You can enroll starting three months before the month of your 65th birthday, or up to three months after.

Miss that window, and the consequences are serious. You could face a gap in coverage, and more importantly, you may be charged a late enrollment penalty for the rest of your life. That’s not a typo. It’s a permanent surcharge added to your monthly premium — a detail that isn’t widely advertised and catches many people completely off guard.

So, mark the calendar. Set a reminder. Don’t let the deadline sneak up on you.

A Word About Insurance Brokers

Many supplemental plans require working with an insurance broker to enroll. This can be helpful — but go in with your eyes open. Be cautious of brokers who seem overly enthusiastic about enrolling you in a Medicare Advantage plan. They typically earn a higher commission on those plans, and a Medicare Advantage plan may not be the right fit for your situation. Ask questions, compare options, and don’t let anyone rush you. And most of all, remember, NOTHING IN LIFE IS FREE!

The Income Surprise: What You Earned Two Years Ago Determines What You Pay Today!

This is the part that genuinely surprised us — and the part most people never see coming.

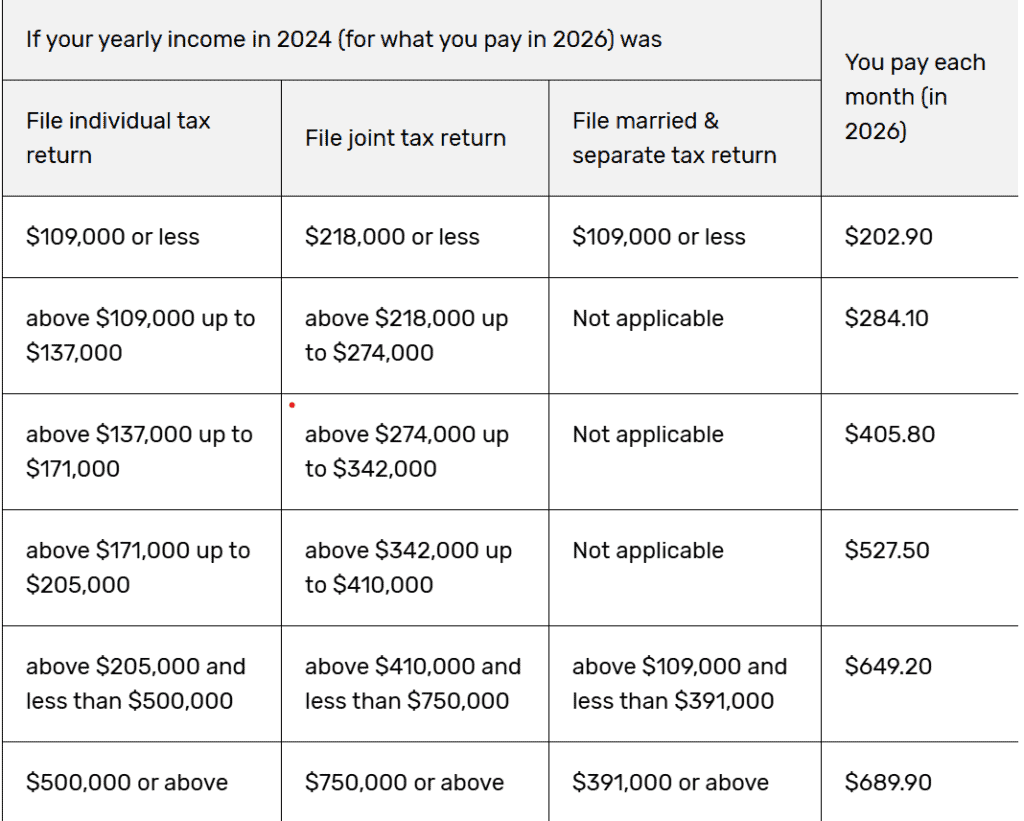

Medicare Part B premiums are not a flat fee for everyone. They are income-based — specifically, based on your Modified Adjusted Gross Income (MAGI) from your tax return two years prior to your Medicare start date.

For 2026 Medicare premiums, that means Medicare is looking at your 2024 income.

The base premium is $202.90 per month. But for households that earned more than $109,000 in 2024, premiums increase on a sliding scale. At the higher end of the income spectrum, that monthly Medicare premium reaches $689.90 per person. (See the 2025 IRMAA chart below.)

Why does this catch people off guard? Because those two prior years are often peak earning years — the final stretch of a career when salaries, bonuses, and investment income tend to be at their highest. You may have already mentally “left” that income behind, but Medicare hasn’t.

This income-based adjustment is called IRMAA — the Income Related Monthly Adjustment Amount. It’s worth knowing that term, because it will come up again and again in retirement financial planning conversations. And now you know exactly who IRMAA is.

But Here’s the Good News – You Can Fight Back

If you’ve just retired and your income has dropped significantly from what it was two years ago, there’s a form you need to know about: SSA-44. Officially called the Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event form, it allows you to ask Social Security to recalculate your IRMAA using your current, lower income rather than that two-year-old number. Retirement qualifies as a life-changing event — specifically what the SSA calls a “work stoppage” — and it’s one of the most common and legitimate reasons to file an appeal. If your appeal is approved, any excess premiums you’ve already paid will be reimbursed, and your future premiums will automatically reflect the lower recalculated amount. You’ll need to provide documentation — a retirement letter, final pay stub, or similar evidence — along with your best estimate of your current year’s income. One important timing note: don’t submit the form until you’ve received your IRMAA Determination Letter stating you’re subject to IRMAA. Each spouse must file their own form separately. This won’t eliminate IRMAA for everyone, but if your income has dropped meaningfully since those peak earning years, it’s absolutely worth the effort.

How Much Does Medicare Really Cost in Retirment?

When you add it all together — Part B premiums, a drug plan, a supplemental plan, and dental and vision coverage — the monthly cost of healthcare in retirement can easily reach $1,000. For couples, that number doubles.

That’s a significant line item that many retirement budgets don’t fully account for — and one of the most common reasons retirees find themselves financially stretched in their first years out of the workforce.

What You Can Do Now: Planning Ahead for Medicare Costs

The good news is that with some advance planning, there are ways to manage these costs. A few things worth discussing with your financial advisor:

Review your projected income in the two years before Medicare begins. Strategic decisions about Roth conversions, capital gains timing, or retirement account withdrawals could affect your IRMAA bracket — and potentially save you hundreds of dollars a month.

Understand your enrollment window and don’t miss it. A lifetime penalty is a steep price for a missed deadline.

Shop supplemental plans carefully. Costs and coverage vary more than you’d expect, and the right plan depends on your health, your doctors, and your budget.

Budget realistically for healthcare. It will likely be one of your largest retirement expenses. Plan for it accordingly — including dental and vision.

Medicare isn’t bad. For most of us, it will be an essential and valuable part of retirement life. Going in with clear eyes — knowing exact costs, how those costs are calculated — makes all the difference.

Frequently Asked Questions:

What is IRMAA? IRMAA stands for Income Related Monthly Adjustment Amount. It’s an additional surcharge added to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. For 2026, that threshold starts at $109,000 for individuals.

What is the Medicare Part B premium for 2026? The base Medicare Part B premium for 2026 is $202.90 per month. However, higher-income beneficiaries may pay significantly more — up to $689.90 per month — due to IRMAA adjustments.

Does Medicare cover dental and vision? No. Traditional Medicare does not cover routine dental or vision care. You will need to purchase separate standalone plans or pay out of pocket for these services.

When should I sign up for Medicare? You can enroll starting three months before the month of your 65th birthday, or up to three months after. Missing this window can result in delayed coverage and a permanent late enrollment penalty.

How do I avoid higher Medicare premiums? Work with a financial advisor in the years before you turn 65 to manage your taxable income. Strategies like Roth conversions, timing capital gains, and managing retirement account withdrawals can help keep your MAGI below IRMAA thresholds.

Next in the series: Withdrawal Timing — and why taking money out at the wrong moment can permanently shrink your retirement savings.

Or check out if you are ready for retirement: Are you ready for Retirement?