Building a retirement income portfolio isn’t just about finding yield – it’s about structuring income in a way that can generate reliable income while protecting what you’ve built.

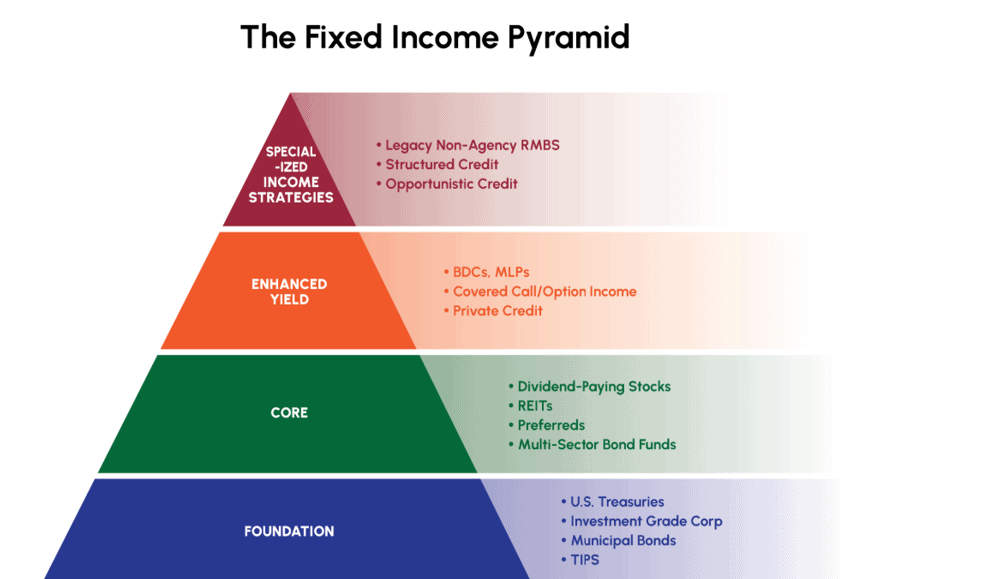

One helpful way to think about this is through a Fixed Income Pyramid.

At the base (Foundation) are the most reliable sources of income—assets designed to preserve capital and generate steady, contractual cash flow. This includes instruments like U.S. Treasuries, investment-grade corporate bonds, municipal bonds, and TIPS.

The middle layer (Core) introduces assets that still generate income but add some variability and growth potential. These include dividend-paying stocks, REITs, preferred securities, and multi-sector bond funds.

Above that, the Enhanced Yield layer consists of higher-income strategies that come with greater complexity and risk—such as BDCs, MLPs, covered call strategies, and private credit.

At the very top are Specialized Income Strategies—targeted, opportunistic allocations like legacy non-agency RMBS and structured credit. These can enhance income, but require deeper expertise and should generally represent a smaller portion of a retiree’s portfolio.

The goal of this framework is simple: Build your income from the bottom up—prioritizing stability first, then layering in yield and complexity where appropriate.

Focusing initially on the Foundation, investment-grade corporate bonds play a key role. They help anchor the portfolio with dependable income while typically offering more yield than Treasuries alone.

Investment-Grade Corporate Bonds

1. What Asset Class Is

Investment-grade corporate bonds are loans made by investors to financially strong companies. Firms like Apple Inc. or Johnson & Johnson issue these bonds to raise capital, and in return, investors receive regular interest payments.

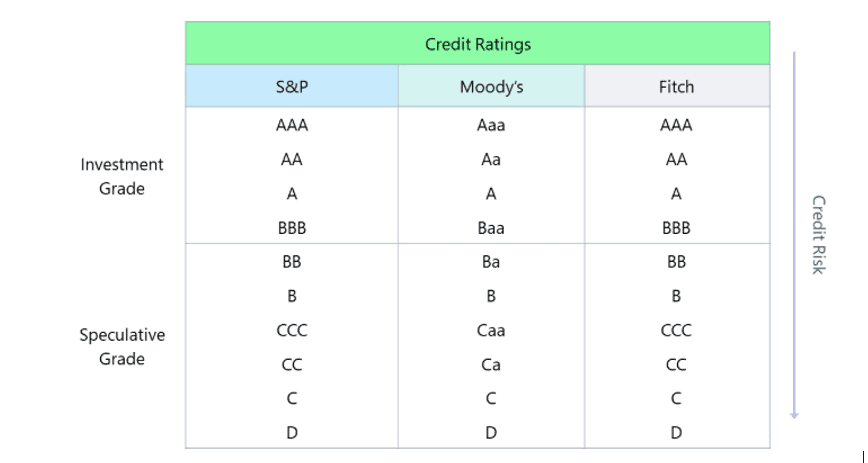

“Investment-grade” simply means the company has a high credit rating—typically BBB- or higher—from agencies like Standard & Poor’s or Moody’s. These are considered relatively low risk compared to lower-rated (high-yield) bonds.

Income comes in the form of fixed interest payments, usually paid semiannually, with the principal returned at maturity.

In plain terms: You’re lending money to strong companies and getting paid predictable interest in return.

2. Why Retirees Use It

Investment-grade corporates sit at the heart of many retirement portfolios because they offer a balance of income and stability.

Retirees use them to:

- Generate predictable income typically higher than U.S. Treasuries

- Add credit diversification beyond government bonds

- Reduce reliance on stock dividends

- Provide a buffer against equity market volatility

They tend to work best when:

- Economic conditions are stable or improving

- Default risk is low

- Investors want more income without taking on equity-level risk

Why it matters: This is one of the simplest ways to turn savings into a steady paycheck without stepping too far out on the risk spectrum.

3. What the Income Actually Looks Like

Investment-grade corporate bonds are designed for consistency—not maximum yield.

| Metric | Typical Range |

| Yield | ~4% – 6% (varies with rates) |

| Payment Frequency | Semiannual (sometimes quarterly via funds) |

| Income Stability | High |

| Volatility | Low to Moderate |

A few important notes:

- Individual bonds pay fixed coupons

- Bond funds smooth income but may vary slightly over time

- Yields move with interest rates—today’s opportunity set may differ from a few years ago

Reality check: You’re trading a bit of yield for a higher degree of reliability.

4. What Can Go Wrong

Even high-quality bonds carry risk. The key is understanding where the cracks can form.

- Interest Rate Risk

When rates rise, bond prices fall. This was clearly demonstrated during the 2022 bond market selloff, when even high-quality bonds experienced meaningful declines. - Credit Risk

While rare, companies can be downgraded or, in extreme cases, default. Investment-grade bonds are not risk-free. - Spread Widening

During economic stress, the extra yield (credit spread) investors demand can increase, pushing prices lower (remember bonds are sold on price)—even if the company remains healthy. - Inflation Risk

Fixed payments lose purchasing power during periods of elevated inflation. - Liquidity Risk

In stressed markets, corporate bond trading can become less liquid, amplifying price swings.

Bottom line: You’ll likely get your income, but the market value can move more than many retirees expect.

5. How It Behaves in Different Markets

Understanding behavior is key to proper portfolio use.

- Rising Rates: Prices decline, but reinvestment opportunities improve over time

- Recessions: Prices may fall due to widening credit spreads, though defaults in investment-grade remain low

- Equity Bear Markets: Often holds up better than stocks, but not always a perfect hedge

- Inflationary Periods: Can lag, as fixed payments lose real value

Unlike Treasuries, corporate bonds are partially tied to economic health.

Translation: They don’t fully “zig” when stocks “zag”—but they usually fall less.

6. How Much a Retiree Might Own

Investment-grade corporates are typically a core allocation, not a satellite.

| Investor Type | Allocation |

| Conservative | 20–40% |

| Balanced | 15–30% |

| Income-focused | 10–25% |

How they fit:

- Often replace part of a Treasury allocation to enhance yield

- Complement dividend stocks by providing contractual income

- Anchor the “40” in a traditional 60/40 portfolio

7. The Bottom Line (Sleep-At-Night Test)

Good fit for:

- Retirees seeking steady, predictable income

- Investors who want moderate yield without equity-level risk

- Those building a diversified income foundation

Less ideal for:

- Investors needing guaranteed principal (use Treasuries instead)

- Those highly sensitive to interim price fluctuations

- Investors seeking high income above all else

Key Takeaway:

Investment-grade corporate bonds are a dependable, middle-of-the-road income source—steady enough to anchor a portfolio. But like any asset class are not without potential bumps along the way.

Disclaimer: This Blog Post is for general information and entertainment purposes only. Readers are encouraged to consult with qualified professionals before making decisions based on the content provided. We are not responsible for any losses, damages or inconveniences caused by the use of this blog content.